Using Gradient Boosting for Regression Problems

Introduction :

The goal of the blogpost is to equip beginners with basics of gradient boosting regressor algorithm and quickly help them to build their first model. We will mainly focus on the modeling side of it . The data cleaning and preprocessing parts would be covered in detail in an upcoming post.

Gradient Boosting for regression builds an additive model in a forward stage-wise fashion; it allows for the optimization of arbitrary differentiable loss functions. In each stage a regression tree is fit on the negative gradient of the given loss function.

The idea of boosting came out of the idea of whether a weak learner can be modified to become better.A weak hypothesis or weak learner is defined as one whose performance is at least slightly better than random chance. The objective is to minimize the loss of the model by adding weak learners using a gradient descent like procedure. This class of algorithms were described as a stage-wise additive model. This is because one new weak learner is added at a time and existing weak learners in the model are frozen and left unchanged.

Gradient boosting involves three elements:

- A loss function to be optimized.

- A weak learner to make predictions.

- An additive model to add weak learners to minimize the loss function.

- Loss Function

The loss function used depends on the type of problem being solved. It must be differentiable. Regression may use a squared error.

- Weak Learner

Decision trees are used as the weak learner in gradient boosting.

Specifically regression trees are used that output real values for splits and whose output can be added together, allowing subsequent models outputs to be added and “correct” the residuals in the predictions.

Trees are constructed in a greedy manner, choosing the best split points based on purity scores.

- Additive Model

Trees are added one at a time, and existing trees in the model are not changed.

A gradient descent procedure is used to minimize the loss when adding trees.

Traditionally, gradient descent is used to minimize a set of parameters, such as the coefficients in a regression equation or weights in a neural network. After calculating error or loss, the weights are updated to minimize that error.

Instead of parameters, we have weak learner sub-models or more specifically decision trees. After calculating the loss, to perform the gradient descent procedure, we must add a tree to the model that reduces the loss (i.e. follow the gradient). We do this by parameterizing the tree, then modify the parameters of the tree and move in the right direction by (reducing the residual loss.

Enough of theory , let’s start with implementation.

Problem Statement :

To predict the median prices of homes located in boston area given other attributes of the house.

Data details

Boston House Prices dataset

===========================

Notes

——

Data Set Characteristics:

:Number of Instances: 506

:Number of Attributes: 13 numeric/categorical predictive

:Median Value (attribute 14) is usually the target

:Attribute Information (in order):

– CRIM per capita crime rate by town

– ZN proportion of residential land zoned for lots over 25,000 sq.ft.

– INDUS proportion of non-retail business acres per town

– CHAS Charles River dummy variable (= 1 if tract bounds river; 0 otherwise)

– NOX nitric oxides concentration (parts per 10 million)

– RM average number of rooms per dwelling

– AGE proportion of owner-occupied units built prior to 1940

– DIS weighted distances to five Boston employment centres

– RAD index of accessibility to radial highways

– TAX full-value property-tax rate per $10,000

– PTRATIO pupil-teacher ratio by town

– B 1000(Bk – 0.63)^2 where Bk is the proportion of blacks by town

– LSTAT % lower status of the population

– MEDV Median value of owner-occupied homes in $1000’s

:Missing Attribute Values: None

:Creator: Harrison, D. and Rubinfeld, D.L.

This is a copy of UCI ML housing dataset.

http://archive.ics.uci.edu/ml/datasets/Housing

This dataset was taken from the StatLib library which is maintained at Carnegie Mellon University.

The Boston house-price data of Harrison, D. and Rubinfeld, D.L. ‘Hedonic prices and the demand for clean air’, J. Environ. Economics & Management, vol.5, 81-102, 1978. Used in Belsley, Kuh & Welsch, ‘Regression diagnostics

…’, Wiley, 1980. N.B. Various transformations are used in the table on pages 244-261 of the latter.

The Boston house-price data has been used in many machine learning papers that address regression

problems.

Tools used :

Pandas , Numpy , Matplotlib , scikit-learn

Python Implementation with code :

Import necessary libraries

Import the necessary modules from specific libraries.

import numpy as np import pandas as pd %matplotlib inline import matplotlib.pyplot as plt from sklearn.model_selection import train_test_split from sklearn import datasets from sklearn.metrics import mean_squared_error from sklearn import ensemble

Load the data set

Use pandas module to read the taxi data from the file system. Check few records of the dataset.

# ############################################################################# # Load data boston = datasets.load_boston() print(boston.data.shape, boston.target.shape) print(boston.feature_names)

(506, 13) (506,) ['CRIM' 'ZN' 'INDUS' 'CHAS' 'NOX' 'RM' 'AGE' 'DIS' 'RAD' 'TAX' 'PTRATIO' 'B' 'LSTAT']

data = pd.DataFrame(boston.data,columns=boston.feature_names) data = pd.concat([data,pd.Series(boston.target,name='MEDV')],axis=1) data.head()

CRIM ZN INDUS CHAS NOX RM AGE DIS RAD TAX PTRATIO B LSTAT MEDV 0 0.00632 18.0 2.31 0.0 0.538 6.575 65.2 4.0900 1.0 296.0 15.3 396.90 4.98 24.0 1 0.02731 0.0 7.07 0.0 0.469 6.421 78.9 4.9671 2.0 242.0 17.8 396.90 9.14 21.6 2 0.02729 0.0 7.07 0.0 0.469 7.185 61.1 4.9671 2.0 242.0 17.8 392.83 4.03 34.7 3 0.03237 0.0 2.18 0.0 0.458 6.998 45.8 6.0622 3.0 222.0 18.7 394.63 2.94 33.4 4 0.06905 0.0 2.18 0.0 0.458 7.147 54.2 6.0622 3.0 222.0 18.7 396.90 5.33 36.2

Select the predictor and target variables

X = data.iloc[:,:-1] y = data.iloc[:,-1]

Train test split :

x_training_set, x_test_set, y_training_set, y_test_set = train_test_split(X,y,test_size=0.10, random_state=42, shuffle=True)

Training / model fitting :

Fit the model to selected supervised data

# Fit regression model

params = {'n_estimators': 500, 'max_depth': 4, 'min_samples_split': 2,

'learning_rate': 0.01, 'loss': 'ls'}

model = ensemble.GradientBoostingRegressor(**params)

model.fit(x_training_set, y_training_set)

Model parameters study :

from sklearn.metrics import mean_squared_error, r2_score

model_score = model.score(x_training_set,y_training_set)

# Have a look at R sq to give an idea of the fit ,

# Explained variance score: 1 is perfect prediction

print('R2 sq: ',model_score)

y_predicted = model.predict(x_test_set)

# The mean squared error

print("Mean squared error: %.2f"% mean_squared_error(y_test_set, y_predicted))

# Explained variance score: 1 is perfect prediction

print('Test Variance score: %.2f' % r2_score(y_test_set, y_predicted))

R2 sq: 0.9798997042218072 Mean squared error: 5.83 Test Variance score: 0.91

Accuracy report with test data :

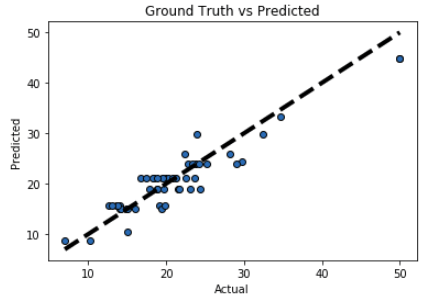

Let’s visualise the goodness of the fit with the predictions being visualised by a line

# So let's run the model against the test data

from sklearn.model_selection import cross_val_predict

fig, ax = plt.subplots()

ax.scatter(y_test_set, y_predicted, edgecolors=(0, 0, 0))

ax.plot([y_test_set.min(), y_test_set.max()], [y_test_set.min(), y_test_set.max()], 'k--', lw=4)

ax.set_xlabel('Actual')

ax.set_ylabel('Predicted')

ax.set_title("Ground Truth vs Predicted")

plt.show()

Conclusion :

We can see that our R2 score and MSE are both very good. This means that we have found a best fitting model to predict the median price value of a house. There can be further improvement to the metric by doing some preprocessing before fitting the data. However the task for the post was to provide you sufficient knowledge to implement your first model. You can build over the existing pipeline and report your accuracies.